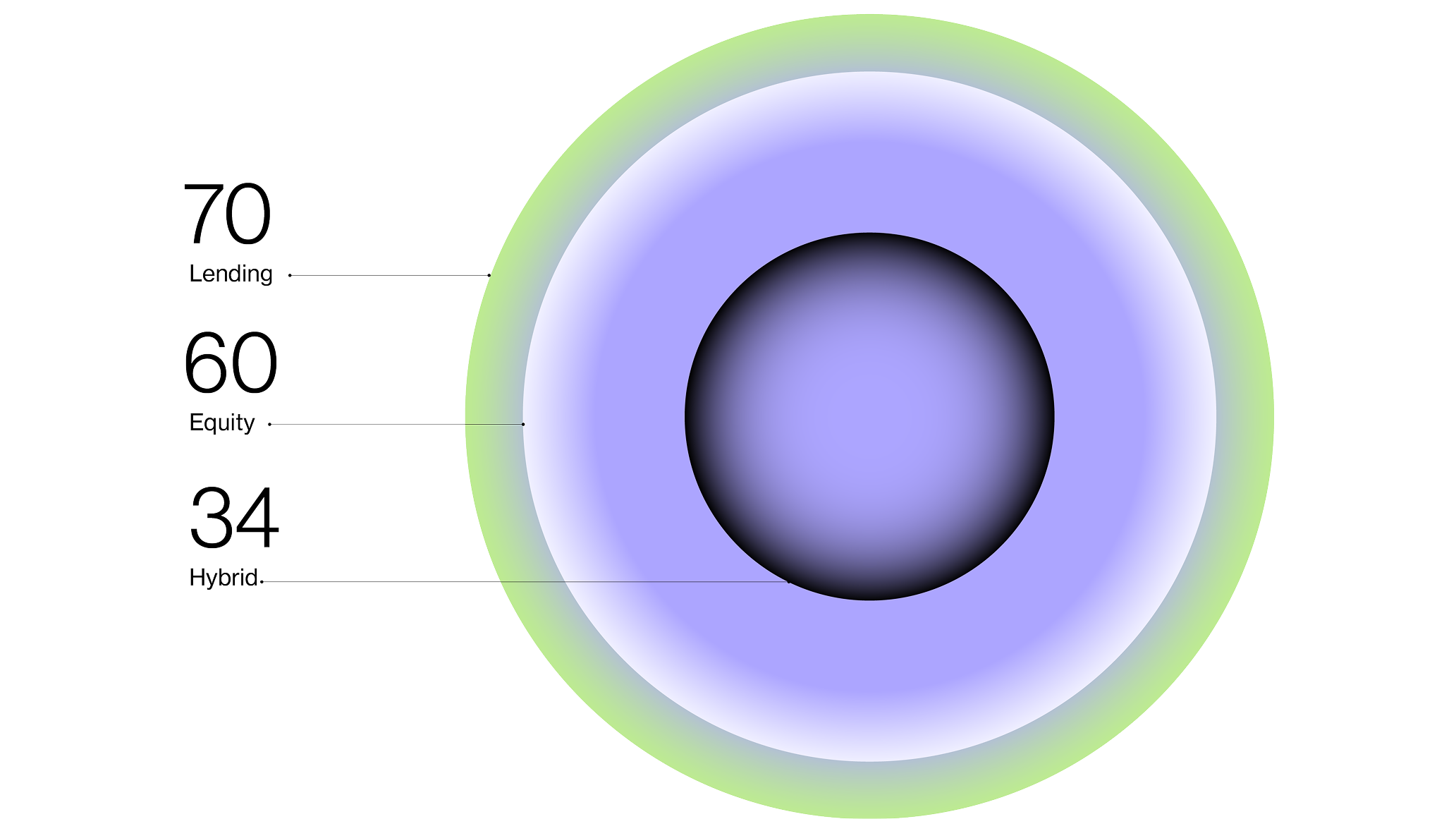

This independent research identifies the elements needed to fully understand the real estate crowdfunding market, its players and trends by looking at the activity of the main platforms, their performance and the characteristics of the projects funded.